Economics SS2 Third Term

Economics SS2 Third Term

Economics SS2 Third Term

PUBLIC FINANCE AND FISCAL POLICY

CONTENT

- Public Finance

- Fiscal Policy

- Revenue Allocation in Nigeria

- Government Revenue and Expenditure

Economics SS2 Third Term

Public Finance

Meaning of Public Finance

Public finance deals with the financial activities of government with respect to revenue and expenditure. It shows government policy measures on generating revenue (income) and allocating expenditure, borrowing and lending, receiving and spending by the federal, state and local governments and their agencies to achieve specific objectives.

Objectives of Public Finance

Public finance aims at the following:

- Effective and efficient allocation of resources among the different sectors of the economy.

- Improving the level of production by reducing tax, granting subsidies and increasing government investment in productive activities.

- Re-distribution of income and productive goods among the various classes in the economy.

- Ensuring price stability by curtailing inflationary and deflationary tendencies in the economy to maintain reasonable prices of goods and services over time.

- Creating an improved and favorable balance of payments through increased taxation, import duties, subsidies, etc

- Creation of employment opportunities thereby reducing the level of unemployment to the barest minimum.

- Development of a good and appropriate fiscal policy for the government.

- Promotion of social welfare through the provision of infrastructural goods at reduced prices.

- Revenue generation through creation of diverse avenues by which government can derive more revenue.

Fiscal Policy

Meaning of Fiscal Policy

Fiscal policy involves the use of income and expenditure instruments to regulate economic activities. It is the use of government revenue through taxation and other sources with a definite pattern of expenditure to influence the economy.

Objectives of Fiscal Policy

- Fiscal policy can be used by government to attain rapid economic development.

- It can be used for revenue/income generation for government use.

- It can create more job opportunities for the people.

- Industrial growth and development can be achieved through a good fiscal policy.

- Fiscal policy can be useful in the allocation or redistribution of a country’s resources or wealth.

- It can enhance higher productivity level of workers.

- Inflation can be controlled e.g. through increased taxation on personal income, reduced government spending, etc.

- A good fiscal policy can enhance balance of payment equilibrium. For instance, government can impose tariff on some imported good to conserve scarce foreign exchange.

EVALUATION

- What is public finance? List 5 of its objectives.

- Briefly explain fiscal policy.Enumerate 5 of its objectives.

Revenue Allocation in Nigeria

Revenue allocation is the process of sharing the nation’s annually generated revenue among the various levels of government i.e. Federal, State and Local governments.

In Nigeria, various commissions were set up over the years to resolve the problems arising from revenue allocation. These include:

- The Phillipson Commission (1946)

- Hicks – Phillipson Commission (1951)

- Chick Commission (1953)

- Raisman Commission (1958)

- Binns Commission (1964)

- Dina Commission (1968)

- Aboyade Commission (1977)

- Okigbo Commission (1979)

- National Revenue Mobilization Allocation and Fiscal Commission (1989).

In all, each of these commissions came up with a formula thought to be workable in allocating the centrally-collected revenue among the different levels of government. These formulae were based on some principles.

Principles of Revenue Allocation in Nigeria

The principles used by one or the other of the revenue allocation commissions include the following:

- Principle of Derivation: That states from which a source of revenue is obtained should receive an extra share over and above others.

- Even Development: Spreading growth and development in a way to reduce inequality among states and local governments.

- Population: Consideration to be given to population strengths of states.

- Land Mass: That states with large expanses of land would require more revenue to develop the land resource.

- Equality of States: This principle views states as being equally created. Therefore, they should be equally empowered.

- Need: that needs of individual states should be given consideration in sharing national revenue.

- Absorptive or utilization capacity: That revenue should be allocated on the basis of how each state is able to efficiently utilize them.

- National interest: This is used by the highest level of government on discretion to allocate funds to lower levels or units to serve diverse needs and considerations.

One or more of these principles have been used by the various commissions over the years to come up with different formulae as in the table below:

| Year | Federal (%) | State (%) | Local (%) | Special (%) | |

| 1977 | 60 | 30 | 10 | — | |

| 1979 | 53 | 30 | 10 | 7 | |

| 1987 | 40 | 40 | 20 | — | |

| 2002 | 48.5 | 24 | 20 | 7.5 | |

| 2003 | 46.63 | 33 | 20.37 | — | |

Government Revenue and Expenditure

Government Revenue

Government (Public) revenue is the total income accruing to the government at all levels (federal, state, local) from various sources to run the country.

This can be in the form of Capital Revenue or Recurrent Revenue

Capital Revenue

This is revenue from irregular sources for meeting expenditure on heavy capital projects e.g. Grants, loans tied to a project, transfers from current revenue, etc.

Recurrent Revenue

This is revenue from regular sources e. g. taxation, fees, licenses, fines, interests on loans, etc.

Sources of Government Revenue

- Taxes on individuals and corporate bodies in form of direct or indirect taxes.

- Loans – Government can obtain loans from internal and/or external sources to execute projects.

- Fees, Fines, Charges and Licenses – These include court, visa and passport fees, vehicle license, postage charges, etc

- Rents, Rates and Royalties – Government also earns revenue from water buildings and properties owned by the government. Royalties are revenue from the mining sector of the economy.

- Grants and aids from foreign countries and international bodies or financial organizations e.g. World Bank, UNICEF, etc.

- Interests, dividends and profits from government directly investments.This is revenue from government-owned business enterprises or joint ventures.

- Others – Other sources of income include levies, penalties, donations, disposal of assets, etc.

Government Expenditure

Government expenditure refers to the total expenses incurred by public authorities at all levels of administration (federal, state, local) in the country. This includes both recurrent and capital expenses.

Economics SS2 Third Term

Capital Expenditure

Capital expenditure are expenses on long-term capital projects e.g. roads, bridges, schools, hospitals, industries, sinking of bore holes, building of offices, etc.

Recurrent Expenditure

These are expenses on the day-to-day running of activities of government which are not permanent in nature. These include expenses on salaries, bills, stationeries, maintenance and repair of infrastructures, etc.

Items of Government Expenditure

There are different areas and sectors which government expends on. These include the following:

- General administration: Areas requiring government spending include:

- the civil service

- the legislature

- the judiciary

- the executive

- embassies outside the country

- political appointees

- other government departments and parastatals

- Economic services which include agriculture, trade, industry, commerce, mining, communication, forestry, power, etc.

- Social services including infrastructures (roads, hospitals, electricity, water, etc), education, health-care delivery, markets, recreational facilities, environmental sanitation, etc.

- Defence and national security: Training and maintenance of armed forces (army, navy, air-force) and the police.Government also expends on arms and ammunitions to ensure the protection of its citizenry.

- Transfer services: These are expenses on servicing of government/public debts, payment of pensions and gratuities, loans to local authorities and friendly nations, grants and aids, etc.

EVALUATION

- Differentiate between capital revenue and recurrent revenue; capital expenditure and recurrent expenditure.

- List and explain five sources of government revenue.

- Enumerate with examples five items of government expenditure.

- Explain government expenditure.

- Mention and explain three items of government expenditure.

- List 5 sources of government revenue.

- Differentiate between government revenue and government expenditure.

- List 5 items under government capital expenditure

TAXATION

CONTENT

- Definition of Tax

- Uses of/Reasons for/Importance of Taxation

- Systems of Tax

- Types/Classification of Tax

- Calculations on Revenue, Expenditure and Tax

Economics SS2 Third Term

Definition of Tax

Tax is a compulsory levy imposed by the government, paid on income and gains occurring to individuals and organization as well as production and consumption of goods and services, and disposal of properties for the common good of all

It is the compulsory payment made by individuals and organizations to the government in order to meet her expenditure.

Uses of/Reasons for/Importance of Taxation

Taxes are collected for the following reasons:

- Revenue Generation: The main purpose of imposing taxes is to generate revenue for financing government activities.

- Discourage consumption of certain goods: Certain goods like tobacco, alcohol are considered harmful to the health of the people, hence government impose heavy tax on them.

- Control and stabilize the economy: Taxes are imposed to control and stabilize the economy especially during inflation and recession. During inflation, taxes are raised to reduce the disposable income and reduce taxes to increase disposable income during economy down-turn.

- Redistribute income: Government can through progressive tax reduce income

- Promotion of economic growth: If government wants to increase output, it reduces tax paid by companies or give tax holiday to infant industries. It will increase employment generation and expansion of the economy.

- Control of balance of payment problem: If important bill is higher than export, balance of payment deficit will arise. Tax on imports will reduce imports and encouragement of export will bail the country out of its financial difficulties.

- Prevention of dumping: Tax increase on imports will prevent dumping of cheap and undesirable goods into the local market.

- Protection of infant industries: Newly established industries are protected from stiff competition from imported goods. Taxes on imported goods are increased, while home industries are granted tax exemption or tax holiday. Home industries can survive.

- Improvement in employment generation: Government can introduce tax cut to stimulate demand and increase output. This promotes employment for the teeming jobless youths.

Systems of Tax

There are three systems of tax. They are: (i) progressive (ii) proportional tax (iii) regressive tax

- Progressive Tax

A tax is progressive if the rate increases as income increases. An individual with high income pays more than a low income earner. Percentage or rate of tax increase as income increases. Example personal income tax was known as Pay As You Earn (PAYE). It can be explained diagrammatically as below

There is direct (positive) relationship between income and tax rate. The higher the income, the higher the tax paid.

Example: A man earns N5,000 and pays 3% which is N 50. The other earns N50,000 and he pays 10% which is N5,000.

Advantages of Progressive Tax

- It is based on ability to pay

- It is productive and assures stable income for the government

- It is equitable: High income earners pay more while low income earners pays less.

- It is economical: The cost of and collecting it is low and easy.

Disadvantages of Progressive Tax

- Tax evasion: Potential tax payers like politicians and business tycoons are notable tax evaders.

- Injustice: High income earners study and work very hard and deserve to enjoy their sweat instead of punishing them with high taxes.

- Discourage capital formation: Progressive tax discourages savings and investment.

- It is arbitrary: There is no standard or yardstick for fixing rate of tax. For example, the then government of Osun state in 1999 to 2000 deducted about 10% from the salary of all workers.

- Proportional Tax

This is a system of tax in which the same rate is charged every tax payer irrespective of the level of income. If the tax rate is 5%, a person earning N2,000 pays N100, N10,000 pays N500 and 50,000 pays N2,500. It can be explained graphically as below:

Economics SS2 Third Term

Advantages of Proportional Tax

- It is simple and easy to understand by all

- It is easy to calculate

- It does not affect pattern of income distribution

Disadvantages of Proportional Tax

- It breeds inequality

- It is less productive: It brings less income to the government

- Has negative impact on the economy

Economics SS2 Third Term

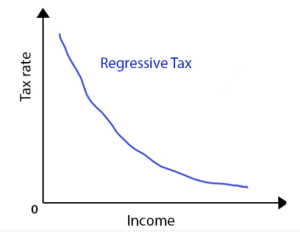

- Regressive Tax

This is a system in which tax rate decreases as income increases. Higher income earners pay less tax than low income earners. Example, sales tax Again, Mr. A. Earns N1,000 and Mr. B earns N4,000 monthly. If Mr. A pays N100 and Mr. B pays N200. Mr. A pays more tax than B because he pays 10% while Mr. B. Though N200, percentage is 5. It can be illustrated below

Types/Classification of Tax

Economics SS2 Third Term

Tax is classified into two. They are 1 direct and 2. Indirect tax

- Direct Tax

This is a tax levied directly on income of individuals and profits of companies by the government.

The burden of tax is borne totally by the tax payer. Examples: personal income tax, capital gain tax, company tax , education tax, poll tax.

Advantages of Direct Tax

- It is equitable and progressive

- Tax payers are aware of how and when to pay the tax

- The cost and time of collecting it is low and short. It is deducted from source – before the payer collects his pay

- Easy and convenient to pay. E.g. P.A.Y.E.

- It is non-inflationary – it does not affect the price system

- It reduces inequality because of its progressive nature

Disadvantages of Direct Tax

- It may discourage production of goods on which taxes are levied. Such taxes will increase their cost of production.

- It reduces the savings ability of tax payers

- It discourages investment as it reduces the amount that companies can plough back into the business.

- It reduces workers disposable income. Hence their purchasing power.

- It is not universal as it is imposed on only some selected sources of income.

- It may lead to tax evasion whereby tax payers fill wrong tax returns to reduce the amount they will pay.

Economics SS2 Third Term

- Indirect Tax

Indirect taxes are taxes levied on production and consumption of goods and services. Examples are custom duties; value added tax, sales tax, etc.

Types of Indirect Tax

- Custom duties: these are in two forms: (a) import duties – taxes imposed on imported goods (b) export duties – taxes levied on a nation’s export goods

- Value Added Tax (VAT): Taxes levied on goods and services at each stage of production.

- Excise duties: Taxes imposed on goods manufactured in a country e.g. beer and cigarette. It is also used to check the consumption of some goods.

- Purchase tax: Imposed on specified goods and paid by wholesalers. It is a percentage of the wholesale price.

Advantages of Indirect Tax

- It is convenient as it is paid when goods and services are purchased

- It has wide coverage – it is paid by almost all income earners.

- It is a source of generating a substantial part of government revenue.

- Less burden on payers as consumers pay in small amounts as they make purchases

- Protection of local infant industries when heavy taxes are imposed on imported goods.

- It is used to correct balance of payment deficit High import duties are used to discourage imports and raise the level of exports.

- Easy and cheap to collect – consumers pay unaware as soon as they buy the taxed commodities.

- They are not easy to evade because the tax has been added the prices of commodities which consumers buy.

- Helps to prevent dumping of cheap and undesirable imported goods in the local market through high import duties.

- It is used to check the consumption of harmful and injurious goods such alcohols and cigarettes. Such commodities are taxed heavily to discourage their production or importation.

- It is a useful tool in implementing government economic policies.

Disadvantages of Indirect Tax

- Indirect taxes are regressive in nature as both high and low income earners pay the same amount on goods purchased.

- They are inflationary in nature as high taxes may increase production costs which will result in high commodity prices. z

- Uncertainty and inaccuracy – the amount to be generated from indirect taxes cannot be easily ascertained.

- It discourages investment: high custom duties on raw materials and finished goods discourage intending investors and reduces the level of production.

- It is difficult to determine the actual tax burden the percentage of tax burden borne by producers, wholesalers/retailers consumers.

- Indirect taxes are difficult to evaluate and remit to appropriate authority by collecting agencies – producers and sellers.

Calculations on Revenue, Expenditure and Tax

The tables below show the expected revenues and projected expenditures from the budget of a hypothetical country in 2016. Use the information in the tables to answer the questions that follow:

Expected Revenue

| ITEM | AMOUNT ($ millions) | |

| Rents, royalties and profits | 75 | |

| Company income tax | 150 | |

| Customs and excise duties | 300.2 | |

| Personal income tax | 80 | |

| Fees and specific charges | 60.8 | |

| Value added tax | 100 | |

Projected Expenditure

| ITEM | AMOUNT (millions) | |

| General administration | 220.1 | |

| Maintenance of foreign missions | 50 | |

| Transfer payments | 65 | |

| Building of schools and hospitals | 200 | |

| Road construction | 180.9 | |

- Calculate the total revenue from: (i) Direct tax (ii) Indirect tax (iii) Non-tax sources

- Determine the total (i) Capital expenditure (ii) Recurrent expenditure

- Determine whether the budget is a surplus or deficit.

Solution

A (i) Direct tax:

Company income tax = 150.00

Personal income tax = 80.00

TOTAL = 230.00

(ii) Indirect tax:

Customs and excise duties = 300.20

Value added tax = 100.00

TOTAL = 400.20

(iii) The revenue from non-tax sources:

Rent, royalties and profits = 75.00

Fees and specific charges = 60.80

TOTAL = 135.80

B (i) Capital expenditure:

Building of schools and hospitals = 200.00

Road construction = 180.90

TOTAL = 380.90

(ii) Recurrent expenditure:

General administration = 220.10

Maintenance foreign mission = 50.00

Transfer payment = 65.00

TOTAL = 335.10

(C) Total Revenue: $766.00 million

Total expenditure = $716.00 million

Surplus = $766 – $716 = $50 million

The budget is a surplus because total revenue exceeds the total expenditure.

Economics SS2 Third Term

EVALUATION

- Give 5 examples in tabular form of direct tax and indirect tax.

- Mention and briefly explain the 3 systems of tax show them graphically.

- What is incidence of taxation?

BALANCED AND UNBALANCED BUDGETS

CONTENT

- Definition of Budget

- Categories of Budget

- Reasons for Balanced Budgets

- Meaning of Surplus and Deficit Budgets

- Ways of Financing Deficit Budget and their Effects

- Effects of Deficit Budget Financing

Economics SS2 Third Term

Definition of Budget

A budget is defined as a statement of projected income sand expenditures of an individual, family, organization and nation over a given period of the Budget can be used as organizational tool that guides the achievement of corporate goals.

Categories of Budget

A budget can be categorized into 2 parts, namely:

(i) Income

(ii) Expenditure

Income

It is made mostly on how much to spend or consume based on how much they may be expecting as

income.

Expenditure

This one exists in a situations where how much is projected to be spent.

When income expected exceeds the expenditure or vice-versa we say we have an unbalanced budget.

However, when the projected income equals the expenditure we say we have a balanced budget.

EVALUATION

- Explain the word budget

- Budget can be used as organizational tool. Discuss

- Define balanced budget

Reasons for Balanced Budgets

There are some reasons why the government has to plan a balanced budget, they are as follows;

- To finance important capital projects e.g. construction of roads, dams etc.

- To finance public goods that would be of benefit to all and sundry.

- To close recession gap.

- To meet current increase in government expenditure.

- To finance economic enterprises that will provide goods this would be self-fiscal policy.

EVALUATION

- What are the reasons why the governments have to plan a balanced budget?

Economics SS2 Third Term

Economics SS2 Third Term

If you need all the content at an affordable price (N500) ONLY, feel free to contact us.

+2348039740135 : whatsapp

Are you a school owner or a teacher,

Click the image below to join Teachers’ Connect to learn more…

YOUR COMMENTS ARE WELCOME